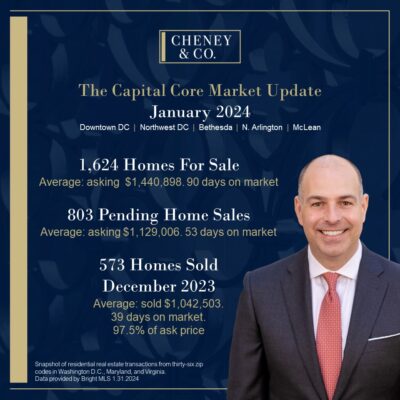

Active listings made a nice improvement (5.52) over the December report. Prices for active listings though shrank slightly (-3.45%) and the days on market for these listings shrank as well since last month (-14.29%).

Pending contracts saw a sizable improvement since last month (21.12%), pricing trended down (-0.97%) and their days on the market contracted as well (-10.17%) to a 53-day average.

Our lagging indicator portion of the report, the December 2023 sales when compared with those from November 2023’s sales, decreased (-10.61%), sold prices eroded slightly (-1.62%), while days on market increased (21.88%), and sellers saw weakening (-2.11%) of their leverage on asking prices (97.5%).

Our take: Supply of homes for sale is on par with past Januarys and we will experience an ever-increasing supply of homes for sale as we enter the Spring Selling Season. On the flip side buyers who took advantage of the seasonal slowdown in November and December were rewarded with concessions by sellers.

The market does appear to be holding its breath for mortgage rates to come down substantially and buyers who seize the day will be rewarded. Sellers who enter the market correctly merchandised will be rewarded too.