The financial case for a well-timed downsize in the DC metro area is almost always stronger than empty nesters expect, and it starts with running the real numbers before committing to a plan.

The kids are gone, and the conversation you and your partner have been quietly having for a year or two is getting more serious. Maybe it is the maintenance that feels like too much. Maybe it is the mortgage that no longer makes sense for a home with four bedrooms you are not using. Maybe it is simply the feeling that the next chapter deserves to be built with intention rather than inertia.

Whatever is driving the conversation, one thing is almost always true: the financial picture is more favorable than most empty nesters in Washington, DC, Bethesda, McLean, Chevy Chase, and across the DC metro area realize until someone actually runs the numbers with them.

This guide is about that moment, running the numbers, understanding the full financial picture of a downsize or move, and building a plan that lets you act with confidence rather than uncertainty. It is written specifically for DC metro homeowners who have built significant equity in their homes and are now deciding how to deploy it wisely in the next stage of their lives.

Real estate is at the center of this conversation, but so is tax planning, investment strategy, retirement positioning, and the kind of honest thinking about what you actually need that most people do not do until they are already in the middle of a transaction. Doing it before, with clear information and enough time, changes every decision that follows.

Why the Financial Opportunity Is Larger Than Most DC Metro Empty Nesters Realize

If you purchased your home in the DC metro area between 1995 and 2010, you are almost certainly sitting on an asset that has appreciated significantly beyond what you paid for it. In neighborhoods like Bethesda, Chevy Chase, McLean, Northwest DC, Georgetown, Spring Valley, and Potomac, long-term homeowners routinely hold $600,000 to $1.5 million or more in equity, sometimes much more, depending on when they purchased and what they paid.

That equity is one of the most powerful financial resources available to a household in the mid-to-late stages of their working years or early retirement. The question is not whether it is valuable. The question is how to use it intentionally.

Many DC metro homeowners have been so focused on the emotional and logistical dimensions of downsizing that they have not fully mapped the financial opportunity. They know the home is worth more than they paid. But they have not yet modeled what a sale actually produces after costs, what happens to that capital if they purchase a smaller home, how the tax treatment of their gain affects their net position, and how the reduction in ongoing housing costs changes their monthly financial picture over a five or ten year horizon.

Walking through that model, even roughly, is often the moment when a decision that felt uncertain becomes clear. The numbers are almost always more compelling than people expect.

Step One: Know What Your Home Is Actually Worth Today

Financial planning for a downsize or move starts with one foundational input: an accurate, current estimate of your home’s market value. Not the Zillow number, not the assessed value on your property tax bill, and not what your neighbor told you they heard a house down the street sold for six months ago. An accurate, current, professionally prepared estimate based on comparable sales, active competition, and the specific characteristics of your property in your specific neighborhood right now.

In the DC metro area, home values vary dramatically by neighborhood, by street, and by property type. A four-bedroom detached home in Chevy Chase, Maryland may be worth significantly more or less than a comparable home in Chevy Chase, DC a few blocks away. A home in Wesley Heights with a large lot and original architectural detail commands a different premium than a similarly sized home in a neighborhood without those attributes. Getting the number right is the foundation of every financial calculation that follows.

A Comparative Market Analysis from an experienced local agent who actively works in your neighborhood is the most reliable free starting point. It should give you a realistic range, an explanation of what drives your home’s value relative to recent sales, and enough context to build a credible financial model around.

Once you have that number, the rest of the financial picture begins to take shape. The proceeds calculation, the tax analysis, the investment modeling, and the monthly cost comparison all depend on starting with an accurate value estimate. Underestimating your home’s value leads to conservative decisions that leave opportunity on the table. Overestimating it produces a financial model that does not match reality when you go to market.

Step Two: Model Your Net Proceeds With Realistic Selling Costs

Gross home value is the starting point. Net proceeds, meaning what you actually walk away with after the costs of selling are accounted for, is the number that drives the financial plan.

In Washington, DC, the total cost of selling a home commonly runs 8 to 10 percent of the sale price, driven in significant part by DC’s relatively high deed transfer taxes. A seller receiving $1.4 million for a home in Spring Valley or Foxhall might net approximately $1.26 million to $1.29 million after commission, transfer taxes, settlement fees, and preparation costs, before mortgage payoff.

In Maryland, sellers in Bethesda, Chevy Chase, and Potomac face combined state and county transfer taxes, recordation fees, commission, and preparation costs that also commonly total 8 to 10 percent. A seller in Bethesda receiving $1.1 million might net approximately $990,000 to $1.01 million before subtracting any remaining mortgage balance.

In Virginia, the seller-side tax burden is meaningfully lower. There is no state transfer tax on sellers, and the grantor’s tax and recording fees combined typically represent 0.15 to 0.25 percent of the sale price. Total selling costs in McLean, Arlington, or Great Falls more commonly fall in the 6 to 8 percent range. A Virginia seller receiving $1.2 million might net approximately $1.10 million to $1.13 million before mortgage payoff.

Subtracting your remaining mortgage balance from the net proceeds figure gives you your actual available equity. That is the number that funds your next purchase, goes into investment accounts, pays down other debt, or some combination of all three. In the DC metro area, for homeowners who purchased fifteen to twenty-five years ago, this figure is often genuinely transformative.

Building a written net proceeds model, even a simple one, before you make any decisions about timing or next steps, is one of the most clarifying exercises available to empty nesters in the DC metro market. An experienced real estate advisor can help you construct one in a single conversation.

Step Three: Understand Your Capital Gains Tax Position Before You Sell

For many DC metro empty nesters, the capital gains dimension of selling a long-held family home is one of the most important financial planning considerations, and one of the most frequently overlooked until it is too late to do anything about it.

Under current federal tax law, individuals selling their primary residence can generally exclude up to $250,000 of capital gain from federal income tax, and married couples filing jointly can exclude up to $500,000, provided they meet the IRS ownership and use requirements. To qualify for the full exclusion, you generally need to have owned and lived in the home as your primary residence for at least two of the five years preceding the sale.

For homeowners in Bethesda, McLean, Georgetown, and Chevy Chase who purchased twenty or more years ago, the capital gain on a sale today can easily reach $700,000, $900,000, or more. The $500,000 married exclusion covers a significant portion of that gain for most couples. But for those with very large gains, or for sellers who are single, widowed, or divorced, the portion of the gain above the exclusion threshold is subject to federal capital gains tax at rates of 15 to 20 percent depending on income, plus the 3.8 percent net investment income tax that applies to higher-income households.

On a $300,000 taxable gain above the exclusion, that exposure can reach $56,000 to $71,000 in federal tax alone, before state income tax in DC, Maryland, or Virginia. That is a meaningful number, and it is one that can sometimes be reduced through planning that happens before the sale closes, not after.

Strategies worth exploring with a qualified tax advisor before you sell include timing the sale in relation to other income events that affect your tax bracket, understanding how the cost basis of your home is calculated including capital improvements made over the years that increase your basis and reduce your taxable gain, and evaluating whether any portion of the home was used for a home office or rental that affects the exclusion calculation.

This is not an area where general information is sufficient. A conversation with a CPA or tax advisor who is familiar with DC, Maryland, and Virginia real estate transactions before you commit to a sale timeline is a worthwhile and often very valuable investment.

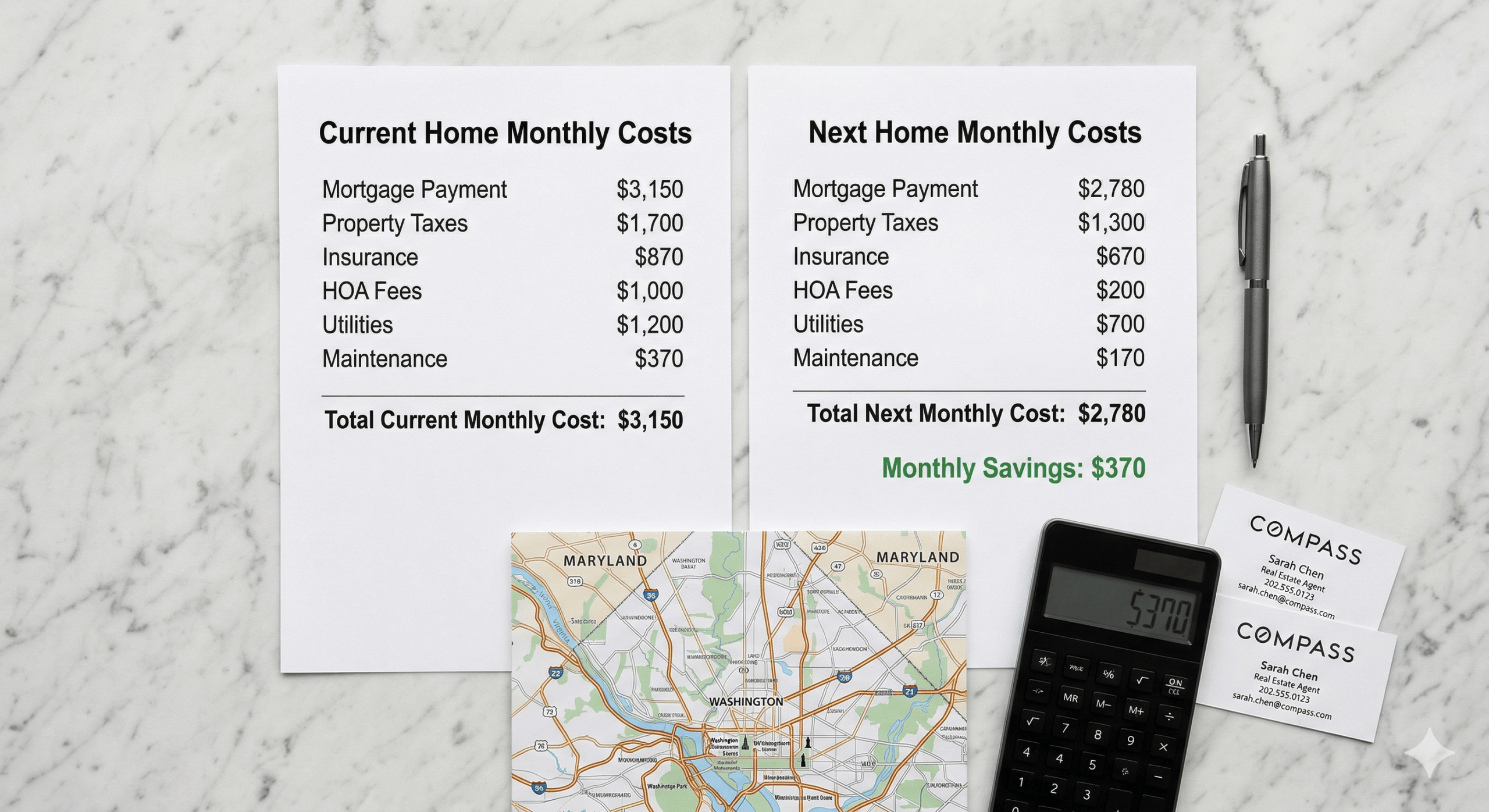

Step Four: Map the Full Monthly Cost Comparison

One of the most concrete and motivating financial exercises an empty nester can do before making a move decision is to map the full monthly cost of their current home against the projected monthly cost of their next one.

This comparison is almost always more favorable than sellers expect, because most people underestimate how many separate costs are embedded in their current housing situation.

For a typical four or five-bedroom family home in Bethesda, McLean, or Northwest DC, the monthly cost picture commonly includes a mortgage payment if the home is not fully paid off, property taxes that in Montgomery County and Northern Virginia can run $800 to $2,000 per month or more depending on assessed value, homeowners insurance, utilities including gas, electric, and water for a larger home, landscaping and yard maintenance, routine maintenance and repair costs that for older DC metro homes often average $500 to $1,000 per month when annualized, and HOA or condo fees if applicable.

Taken together, the full monthly cost of carrying a large family home in the DC metro area at mid to upper price points frequently runs $5,000 to $9,000 per month or more, excluding any mortgage payment on a paid-off home.

The monthly cost of a well-appointed two-bedroom condominium in Bethesda, Friendship Heights, or Arlington typically runs $3,000 to $5,500 per month including HOA fees, taxes, insurance, and utilities, and often with significantly less maintenance burden. A smaller detached home or townhouse in a walkable close-in neighborhood carries a similar or slightly higher cost depending on the specific property and community.

The monthly savings from a downsize, when fully mapped, often produce $1,500 to $4,000 per month in freed cash flow. Over ten years, that represents $180,000 to $480,000 in additional financial flexibility, compounding if invested, or simply available to fund the life you actually want to be living in your next chapter. Combined with the freed equity from the sale itself, the total financial benefit of a well-executed downsize at the right moment in the DC metro market can be among the largest single financial improvements available to a household in their fifties or sixties.

Step Five: Evaluate Your Mortgage and Financing Options for What Comes Next

Empty nesters in the DC metro area who are planning to purchase a smaller home or condominium after selling face a financing landscape that has evolved significantly from what they may remember from their last purchase.

Many empty nesters will have enough equity from their sale to purchase their next home without a mortgage at all, particularly if they are moving to a smaller and lower-priced property. A cash purchase simplifies the transaction significantly, removes appraisal contingency risk, and can be a competitive advantage in certain market conditions. It also eliminates the monthly mortgage payment from the ongoing cost comparison, further improving the monthly financial picture.

For those who choose to finance a portion of their next purchase, the planning conversation should happen well before the home goes to market. Mortgage lenders look at income, assets, and credit profile, and for empty nesters who are transitioning toward retirement, the income picture may look different than it did when they last applied for a mortgage. Retirement income, investment distributions, Social Security, and other income sources are all considered by lenders, but the documentation requirements may be different from what sellers remember.

Getting a pre-approval or at minimum a thorough conversation with a mortgage advisor before you list your current home gives you a clear picture of what your purchase options are on the other side of the transaction. It also helps you structure your timeline intelligently, understanding whether bridge financing is available if needed, and whether the sequence of your sale and purchase needs to be managed in a specific way to optimize your financing position.

Interest rate environment in 2026 should factor into your thinking as well. Rates have been variable in recent years, and locking in favorable terms at the right moment requires having your financing pre-positioned rather than scrambling after a contract is signed.

Step Six: Think Through the Investment of Your Freed Equity

For many DC metro empty nesters, the sale of their family home will produce the largest single influx of capital they have ever managed. Knowing in advance how you intend to put that capital to work is part of financial planning, not an afterthought.

The options range broadly. Some sellers use a portion of the freed equity to pay off all remaining debt, including any mortgage on the new home, car loans, and other obligations, creating a fully debt-free financial position entering retirement. Others invest the capital in diversified investment portfolios, using the proceeds to supplement retirement savings that may not have kept pace with the appreciation of their home. Some use a portion to fund a second property, whether a vacation home in the mountains or at the beach, a rental property that generates income, or a family property that supports multigenerational needs.

There is no single right answer, and the right strategy depends on your retirement timeline, your existing savings, your income picture, and your personal relationship with risk and security. What is clear is that the decision deserves thoughtful consideration before the proceeds hit your account, not after.

Working with a fee-only financial advisor who has experience with real estate transition planning, ideally one who is familiar with DC, Maryland, and Virginia tax contexts, is a worthwhile investment for households managing proceeds in the $500,000 to $1.5 million range. The cost of that advice is typically a small fraction of the value it creates in the decisions it informs.

Step Seven: Build a Timeline That Gives You Room to Execute Well

One of the most consistent patterns I see among empty nesters who execute a downsize well is that they started planning earlier than they thought they needed to. And one of the most consistent sources of stress among those who find the process harder than expected is that they started too late.

A realistic financial planning and execution timeline for an empty nester selling a long-held DC metro family home looks something like this.

Twelve to eighteen months before your target list date, begin the financial planning conversations. Run your net proceeds model. Talk to a tax advisor about your capital gains position. Get a current home value estimate. Start thinking about where you want to go next and what that purchase looks like financially.

Nine to twelve months out, begin the decluttering and sorting process. For a home that has been occupied for fifteen to twenty years, this takes more time than most sellers expect and goes much more smoothly when it is not being done under contract deadline pressure. Begin researching target neighborhoods and property types for your next home. Have a preliminary conversation with a mortgage advisor if you are planning to finance your next purchase.

Six to nine months out, engage your real estate advisor for a pre-listing walkthrough of your current home. Build your preparation plan: what to do, what to skip, and what to spend. Begin scheduling any work, painting, repairs, floor refinishing, staging, that needs to happen before you list. Start attending open houses in your target area to calibrate your expectations against what is actually available at your price point.

Three to six months out, complete your home preparation. Finalize your financing pre-approval if applicable. Coordinate with your advisor on listing timing, taking into account seasonal patterns, current inventory in your neighborhood, and buyer demand conditions. Review your net proceeds model one more time with updated cost estimates.

At listing, your financial plan is already built and your next chapter is already in focus. What remains is execution, which is where an experienced local advisor earns every part of their value.

Mapping the full monthly cost of your current home against your next one is one of the most motivating financial exercises available to DC metro empty nesters, and the savings are almost always larger than expected.

Why This Decision Is Different From Every Financial Decision You Have Made Before

Most financial decisions are reversible. You can change your investment allocation, refinance a loan, adjust your retirement contribution rate, or revisit an insurance policy. The decision to sell your family home is different. Once it is sold, the relationship with that particular piece of your life is complete. The proceeds are in hand. The next chapter has begun.

That irreversibility is not a reason to hesitate. It is a reason to plan carefully, act with confidence, and surround yourself with people who bring genuine expertise to the decisions that matter. A tax advisor who knows DC, Maryland, and Virginia real estate transactions. A financial planner who has worked with clients navigating home sale proceeds. A real estate advisor who has executed hundreds of successful transitions for families in your exact situation, in your exact market, at your price point.

Over 22 years and more than $779 million in career sales across Washington, DC, Maryland, and Virginia, the conversations I value most are the ones that happen early, before a seller is committed to a timeline, when there is still room to plan, adjust, and optimize. The sellers who do best financially are almost never the ones who moved fastest. They are the ones who built the clearest plan.

A Practical Financial Planning Checklist for DC Metro Empty Nesters

Use this as a starting framework for the conversations you need to have in the months before you list. Not every item will require equal attention in your specific situation, but each one is worth at least a brief review with the appropriate advisor.

Home value: Get a current Comparative Market Analysis from an experienced local agent. Know your realistic value range, not a single number, and understand what drives it in your neighborhood.

Net proceeds model: Build a written estimate of your sale proceeds after commission, transfer taxes, settlement fees, preparation costs, and mortgage payoff. Know the number you are actually working with before you make any downstream decisions.

Capital gains analysis: Talk to a CPA or tax advisor before you list. Understand your adjusted cost basis, your expected gain, how the exclusion applies to your situation, and whether there are any timing or structuring decisions that could reduce your tax exposure.

Monthly cost comparison: Map the full monthly cost of your current home, including mortgage, taxes, insurance, utilities, maintenance, and landscaping, against the projected monthly cost of your next home. The difference is your monthly financial improvement from the move.

Financing review: If you plan to finance your next purchase, get a pre-approval or at minimum a lender conversation before you list. Understand what you can access, on what terms, and whether your income documentation supports the loan size you may need.

Investment planning: If your sale will produce significant freed equity, have a conversation with a fee-only financial advisor about how to deploy it. Do not wait until the proceeds are in your account to start this conversation.

Timeline planning: Work backward from your desired move date. Identify every task that needs to happen before listing and build a realistic schedule that gives each step adequate time. Rushing any part of the preparation process almost always costs more than it saves.

Next home research: Begin attending open houses and reviewing listings in your target neighborhoods and price range at least six months before you plan to buy. Understanding what is available, what it costs, and what trade-offs you are willing to make informs your financial plan as much as any spreadsheet.

Legal and estate considerations: For some empty nesters, a home sale is also an opportunity to revisit estate documents, update beneficiary designations, and ensure that the financial and legal structure of the household reflects the new chapter ahead. A brief conversation with an estate attorney is worth adding to the list for households in this stage of life.

Questions DC Metro Empty Nesters Ask About Financial Planning for a Downsize or Move

How much equity do most DC metro empty nesters have when they downsize in 2026?

It varies by neighborhood and purchase date, but homeowners in established DC metro communities who purchased between 2000 and 2010 commonly hold between $500,000 and $1.5 million in equity or more, depending on the property and location. Neighborhoods like Bethesda, Chevy Chase, McLean, Georgetown, and Northwest DC have delivered among the strongest long-term appreciation in the country, producing meaningful wealth for families who stayed in their homes through the appreciation cycle.

How does capital gains tax work when selling a family home in DC, Maryland, or Virginia?

Under current federal law, individuals can generally exclude up to $250,000 in capital gains from the sale of a primary residence, and married couples up to $500,000, subject to IRS ownership and use requirements. Gains above the exclusion are taxed at federal capital gains rates of 15 to 20 percent depending on income, plus a 3.8 percent net investment income tax for higher-income households. DC, Maryland, and Virginia each have their own state income tax treatment of capital gains. A CPA or tax advisor familiar with DC metro real estate transactions is the right person to model this for your specific situation before you sell.

Should empty nesters pay cash or get a mortgage for their next home after downsizing in DC?

If the equity from your sale is sufficient to purchase your next home without a mortgage, a cash purchase eliminates monthly mortgage payments, simplifies the transaction, and can be a competitive advantage in certain market conditions. For many DC metro empty nesters, this is a realistic option that improves their monthly financial picture significantly. If you prefer to preserve liquidity and invest the freed capital, financing a portion of the next purchase at favorable terms while deploying the remainder into investment accounts is also a sound strategy. The right answer depends on your income, your risk tolerance, and your retirement timeline, and is worth discussing with both a financial advisor and a mortgage professional.

What is the best way to invest the proceeds from selling my family home in the DC area?

There is no single right answer, and the right strategy depends on your financial situation, retirement timeline, existing savings, and personal priorities. Common approaches include paying off all remaining debt to enter retirement debt-free, investing in diversified portfolios that supplement retirement savings, purchasing a smaller investment or vacation property, or some combination. A fee-only financial advisor who has worked with clients managing real estate sale proceeds is the right resource for this conversation. It is worth having before the proceeds are in hand, not after.

How do I calculate my adjusted cost basis for capital gains purposes when selling my DC area home?

Your adjusted cost basis starts with what you originally paid for the home and is increased by the cost of capital improvements made during ownership. Improvements that add to the home’s value, extend its useful life, or adapt it to new uses, such as a kitchen renovation, addition, new roof, HVAC replacement, or major landscaping work, generally qualify as additions to your cost basis and reduce your taxable gain. Routine maintenance and repairs do not increase basis. Keeping records of improvements made over the years of ownership is valuable and can have a meaningful impact on your tax calculation. A CPA can help you reconstruct and document your cost basis before you sell.

How long before selling should DC area empty nesters start financial planning for a downsize?

Twelve to eighteen months before your target list date is the ideal starting point for the financial planning conversations. That window gives you time to run your net proceeds model, talk to a tax advisor, build a preparation plan for your home, research your next neighborhood, and position your financing without pressure. The sellers who find the process most manageable are almost always the ones who started early enough to make decisions thoughtfully rather than reactively.

Do I need a financial advisor to plan a downsize in DC, Maryland, or Virginia?

Not every situation requires a formal engagement with a financial advisor. But for empty nesters managing significant equity, navigating capital gains exposure, and making decisions that will shape their financial picture for the next ten to twenty years, a conversation with a fee-only financial advisor who understands DC metro real estate transactions is often one of the highest-return investments in the entire process. The cost of that advice is typically modest relative to the financial decisions it informs. Your real estate advisor can often help you identify the right professional resources if you do not already have them in place.

What happens to my property taxes if I move from a high-value family home to a smaller home in DC, Maryland, or Virginia?

Property taxes in DC, Maryland, and Virginia are calculated based on assessed value and the applicable tax rate for your jurisdiction. Moving from a higher-assessed family home to a lower-assessed condominium or smaller property almost always produces a meaningful reduction in annual property taxes. In Montgomery County, Maryland, for example, where property tax rates on residential properties run roughly 0.9 to 1.1 percent of assessed value, moving from a $1.2 million family home to a $650,000 condominium can reduce your annual property tax bill by $5,000 to $6,000 or more. This reduction factors directly into the monthly cost comparison and improves the financial case for the move.

A Final Word on Planning Your Financial Future Around a Move That Is Already Overdue

Most empty nesters in the DC metro area who are living in a home that no longer fits their actual life are not waiting because the financial case is weak. They are waiting because the decision feels large, the process feels uncertain, and the emotional weight of leaving a home filled with decades of memory is real.

All of that is understandable. And none of it changes the fact that for most families in Bethesda, Chevy Chase, McLean, Northwest DC, Arlington, and Potomac, the financial opportunity of a well-timed, well-planned downsize is among the most powerful wealth events available to them in the coming years.

The equity is there. The market is favorable in most DC metro neighborhoods for well-positioned sellers. The monthly cost savings are real and compounding. The capital gains exclusion is available to most married couples. And the ability to enter the next chapter of life with greater financial security, lower monthly overhead, and more flexibility is achievable with a clear plan and the right team.

The first step is always the same: a conversation. About what your home is worth, what the move could produce financially, what comes next, and what it would take to get from here to there with confidence and clarity.

If you are thinking about downsizing or making a move in Washington, DC, Maryland, or Virginia and want to start building that picture, that conversation is available to you at no cost and no obligation. It takes about an hour and it changes everything about how you see the decision ahead.

About Matt Cheney

Matt Cheney is a top-producing real estate advisor with Compass in Washington, DC, guiding buyers and sellers across DC, Maryland, and Virginia through high-stakes moves, from luxury sales to estate settlements, downsizing, and divorce-related transactions. With over $779 million in career sales volume and 22 years of experience, including more than two decades working on complex and sensitive real estate situations, Matt is known for calm, strategic guidance and brings hundreds of successful sales to clients seeking clarity and support during life transitions.